By BGV Summer Interns and MBA candidates at the Kellogg School of Management Jenieri Cyrus and Nick Giometti

The 2020 COVID Pandemic has forced the in-person events industry on its heels and has put billions of dollars at risk. Thanks to the world of Virtual Events, many event organizers have been able to replace these in person events with virtual representations. Because much of the world is continuing to see massive shutdowns of businesses and restrictions related to mass gatherings, the Virtual Event space has experienced a boon for much of 2020.

Part II of this blog series explores the key players in the Virtual Events industry and attempts to create frameworks to understand the role Virtual Events will likely play in a Post-COVID world. We assess the Virtual Events experience as it exists today to determine what specific companies need to do to emerge as market leaders.

Key Players/Industry Leaders in the Virtual Events Space

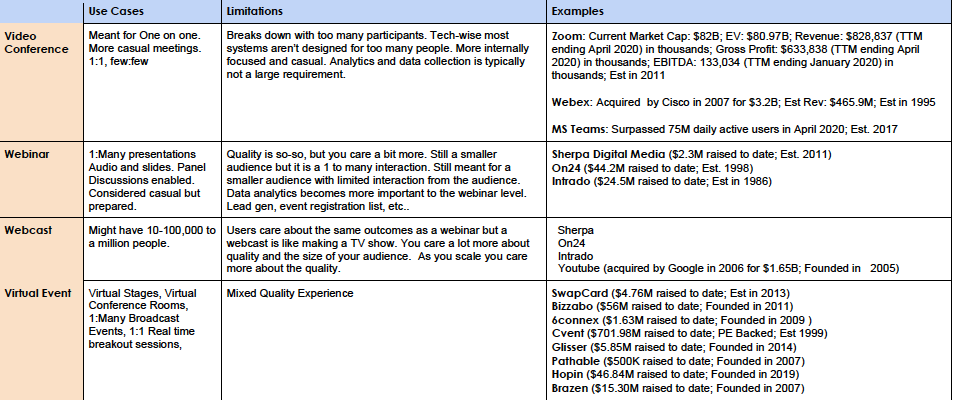

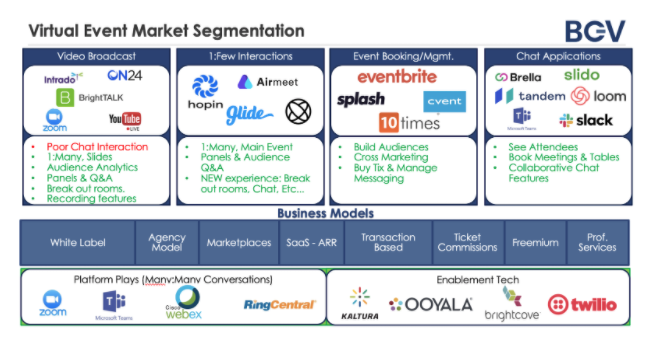

While there are some established virtual event providers such as Cvent (1999) and On24 (1998), the median founding year of virtual event startups is 2012 (based on a sample 56 virtual event providers), which signals that the virtual event space has not fully matured and there remains white space for market winners and incumbents to emerge.Although many of these startups were created to enhance in person events by adding on a digital layer to physical workflows, some providers have proved superiority in terms of virtual event enablement. Others built solutions that optimized for large events and tradeshows. A great way to make sense of this market is to separate the key players into separate buckets based on the use case that their current products satisfy.

Companies within the virtual events vertical can be further segmented with respect to their target customers.

Top of the Funnel/Community Building:

Events in this category are not revenue generating productions, however, they enjoy a high profile, for example job fairs or recruiting events hosted by a university. This specific use case put Brazen on the map. Other events in this category include internal company events put on primarily to foster community within organizations and build camaraderie, or else to source talent and develop new relationships.

Bottom of the Funnel/Revenue Generating:

Trade shows, expos, large conferences and other in-person events that traditionally produce large revenues and profits for major conference organizers comprise this category. Even smaller conferences where attendees pay an entry fee fall into this category as well. Companies like Hopin, Run The World and SwapCard have created virtual event platforms meant to provide solutions for all use cases that fall on this end of the spectrum.

Making the Shift from Physical to Virtual Experience

Technological adaptations:

How can virtual events replicate the in-person experience? More specifically, what technological adaptations are required to capture the feeling of experiencing a large trade show or a conference center?

Platforms like HopIn and SwapCard take the components of live events – check-in, main and side stages, exhibitions, interactive sessions, and scheduled and spontaneous networking – and map them to a digital domain. From the perspective of an attendee, navigating a virtual event platform feels like navigating a web page, with vendors, stages, and interactive sessions all having unique pages and subpages. To make the sites feel more “alive” each page maintains dynamic attendee lists as visitors filter in and out. These exhibitions include both synchronous and asynchronous materials in video, audio, and written formats. Exhibitors can also offer visitors virtual swag through discounts and vouchers to their services.

For large mainstage events, many platforms create spaces to mingle and network pre- and post-presentation. Spontaneous networking constitutes one of the largest tangible benefits of in-person events, and virtual platforms are building scaffolding to replicate random encounters with colleagues or peers from other companies in the same field.

In terms of pure technological adaptations, there are several requirements that are table stakes:

- Video: Virtual event platforms can either provide their own video streaming (Sherpa) or rely on third party providers like Vimeo or Youtube. Without seamless video streaming, the experience is immersion breaking and will lead to users abandoning the platform.

- Cyber security: Information storage is typically done centrally on the platform, and then distributed to vendors post-event. Depending on the amount of PII shared by individuals with the event, virtual event providers need to have robust cybersecurity protocols that meet the regulatory requirements of the participants’ resident countries.

- Asynchronous programming: Because video programming is key to the success of the event, most mainstage presentations require professional production quality AV support. Video production takes additional time to generate high quality segments that survive the event itself and provide evergreen content.

- Data Capture: Traditionally, on-the-ground agents at large events take headcounts of attendees on the floor, and individual exhibitors track attendees through sign-up sheets for follow-up marketing. Virtual events, by contrast, offer a massive advantage in data capture over in-person events, as every interaction with the platform can be recorded and aggregated to form predictive analytics for the event hosts and exhibitors. Building a data capture pipeline is essential to post-event planning and marketing campaigns.

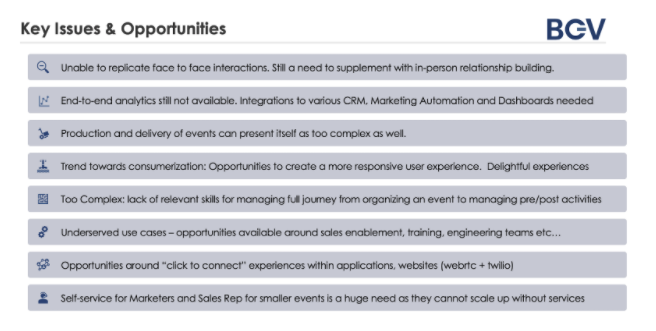

Where we still fall short – Pitfalls of the virtual experience:

- Immersion: Even if we look at large trade shows, deconstruct the individual components, and map them to a virtual interface, something is missing. The whole of the live event experience is greater than the sum of the parts, and the human element brings immediacy and immersion that cannot be replicated virtually. Until VR/AR technology enjoys dramatic improvements and broad adoption, virtual events will need to adapt to improve the user experience.

- Distraction: One of the biggest behavior differences from attending an in-person event versus an virtual one is the ability to disengage. Simply put, if a virtual attendee loses interest in the material, they can walk away from the computer screen. The switching cost is low and demands for a user’s attention during a virtual event are high, making engagement exceptionally important to the success and longevity of virtual event platforms as a medium.

- Lack of Natural Interactions: Human engagement also suffers from the difficulty presented in mimicking spontaneous 1:1 interactions. Mingling, or seeing a familiar face on the floor, presents a remarkable challenge to replicate virtually. As such, virtual event platforms must ensure there is sufficient infrastructure to handle 1:1 video conferencing, private chats, and the ability to hold side-bar conversations during scheduled programming.

New Opportunities Presented by Virtual Events:

Virtual Events, thanks to their digital platform, offer several advantages over in-person alternatives. Specifically, virtual events best in-person events in three areas: Resources, access, and data.

- Resources: Budget for large in-person events can exceed $5M, taking into account costs for production, A/V, travel, permitting, and rent for the venue. Virtual events for an equivalent number of attendees can be done for 10% of the cost. Additionally, total ramp up time for a virtual event can be done in weeks instead of months.

- Access: By circumventing the need to be physically in-person, access opens to a global audience. While virtual ticket pricing struggles to reach an equilibrium with traditional events, global access broadens revenue opportunities. Additionally, programming no longer requires live consumption, meaning lead generation for exhibitors can occur long after a scheduled event.

- Data: Virtual events create a rich corpus of data for both event organizers and exhibitors to improve planning and marketing efforts. Although data is stored at the organizer level for security reasons, exhibitors can generate actionable insights from user behavior while on the event platform. These insights will power ABM, lead generation, and lead scoring in ways previously not known.

A return to the “New Normal” – Hybrid Events and the Return to In-Person:

When events begin to resume in-person, virtual platforms will offer digital infrastructures that enhance the physical experience and provide additional connectivity with virtual attendees. By integrating in-person events with digital infrastructure, in-person attendees will be able to access additional layers of context from physical exhibition booths, and control access to digital content presented on-stage. New forms of connectivity will emerge as virtual attendees will be able to track their friends and colleagues’ location and initiate 1:1 steaming to get a live set of eyes on the ground.

Although the future of physical events remains uncertain, hybrid events will combine the immediacy of physical events, with the supplemental data provided from digital infrastructures to add value for both the event organizers and attendees.

Key Takeaways

Our research highlights several key takeaways, we’d like to leave you with:

- Pre-COVID-19, in-person events and conferences were a $15Bn+ rev/yr market

- The global pandemic spurred the rapid adoption of virtual events technology

- Virtual events are segmented both by function and target customer

- Virtual events provide new opportunities to create value, both for hosts and for attendees, despite current pitfalls

- Because of these new enhancements, the value of virtual events will persist even after returning to physical spaces

As virtual events continue to adapt quickly to our new reality, we look forward to watching which elements endure post-pandemic, and how the space matures and develops in the months and years ahead.